Introduction

Tax season often sneaks up on us, and for many, it’s a time filled with confusion, frustration, and stress. However, by preparing year-round, you can make the entire process smoother, more efficient, and less overwhelming. Managing your finances throughout the year means you will have everything in place when it’s time to file your taxes. In this expanded guide, I’ll break down comprehensive strategies for tax season preparation. Whether you’re a business owner, freelancer, or salaried employee, following these steps will help you stay on top of your finances and save valuable time come tax time.

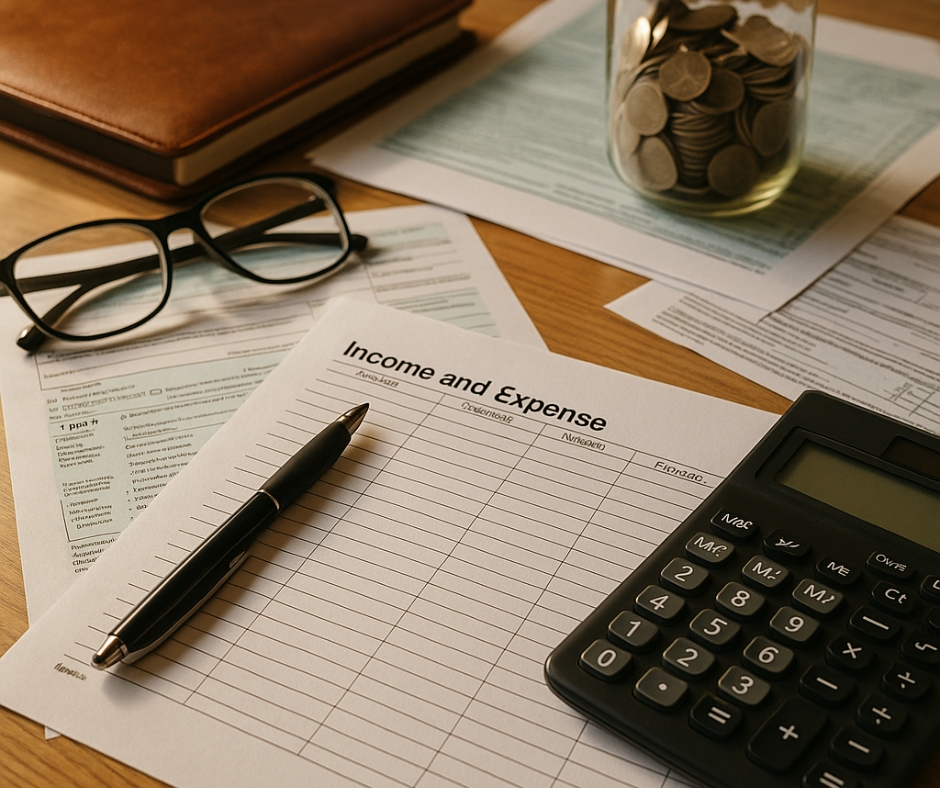

1. Keep Track of All Your Expenses—Consistently and Diligently

Properly tracking your expenses year-round is a fundamental part of tax preparation. The earlier you start this practice, the less likely it is you will miss out on valuable deductions when tax season arrives. As you make purchases, from office supplies to client dinners, keep a record of each one. Utilizing accounting software such as QuickBooks or Xero allows you to seamlessly track income and expenses, generate reports, and even categorize different types of spending. This is especially crucial for businesses and freelancers, as it can help you maximize deductions. Additionally, you should also keep receipts organized—whether you scan them digitally or store them physically. Not only does this help with tax filing, but it also allows you to maintain a clear financial picture throughout the year.

Tracking expenses is more than just about collecting documents; it involves strategic planning. For instance, if you plan to make large purchases that will qualify for a tax deduction, timing them before the year’s end may help reduce your taxable income. Furthermore, maintaining accurate records of any mileage traveled for business or charitable purposes can significantly impact your tax return. The IRS allows deductions for business-related mileage, which can quickly add up, especially for entrepreneurs.

2. Set Aside Money for Taxes—A Habit That Pays Off

Many self-employed individuals and small business owners overlook one of the simplest yet most effective tax season strategies—setting aside a portion of their income for taxes. Far too often, business owners wait until tax season to pay their tax bill, only to face the harsh reality of a large lump sum due. Instead, it’s best to calculate your estimated taxes early in the year and automatically set aside a percentage of each paycheck or business revenue into a dedicated savings account.

This practice prevents tax surprises and allows you to meet your tax obligations without scrambling to find the money at the last minute. The IRS recommends making estimated quarterly tax payments, especially if you are self-employed or run a business. By doing this consistently, you will avoid underpayment penalties and interest on late payments. Having this money set aside will give you peace of mind and make tax time feel more like just another regular task to handle rather than a stressful event. Additionally, this method can help you understand your income flow and set clear goals for your financial health.

3. Understand Your Deductions and Credits—Stay Informed About Tax Laws

Tax laws change regularly, so staying updated on the latest deductions and credits that apply to your situation is crucial. The IRS offers numerous deductions for both personal and business expenses, and these can significantly reduce your taxable income. For businesses, common deductions include operational costs like supplies, software subscriptions, marketing expenses, and even home office space.

One area where many taxpayers miss out is tax credits. Unlike deductions, which reduce the amount of income that is taxable, credits directly reduce your total tax bill. There are credits for everything from education expenses to child care and energy-efficient home improvements. For instance, if you have children, the Child Tax Credit and Child and Dependent Care Credit can significantly lower your overall tax liability. Take the time to research all available credits and deductions relevant to your situation—whether that’s a home-based business, educational expenses, or health savings contributions. You might be surprised at how much you could save.

Beyond knowing your options, it’s essential to stay on top of new tax laws, especially if you’ve recently experienced a major life change such as marriage, divorce, or retirement. Tax laws can impact everything from your filing status to the types of deductions you can claim, so it’s important to review these updates annually.

4. Stay Organized Throughout the Year—Make It a Habit

Organization is perhaps the most important yet underrated part of tax season preparation. Maintaining a well-organized system throughout the year will make the process of gathering documents and filling out forms much easier. Set up a monthly routine where you review and organize your financial documents, categorize your expenses, and update any changes in your income or deductions.

Start by organizing all your receipts, bank statements, and invoices in physical or digital folders. If you are using accounting software, make sure to categorize each transaction appropriately. The goal here is to be as proactive as possible rather than reactive when the deadline approaches. Keeping everything organized prevents the last-minute rush and ensures that nothing gets overlooked, such as a critical expense or deduction. This method also helps if you ever get audited by the IRS, as you will have everything well-documented and easily accessible.

For more in-depth organization, consider creating a tax folder for each tax year. Within this folder, store any receipts, contracts, invoices, and forms that may affect your tax return. This will allow you to stay organized not only during tax season but throughout the year as well. You will appreciate this when you need to refer back to previous years for any reason.

5. Keep Track of Retirement Contributions—Maximize Your Deductions

When it comes to tax season, contributing to your retirement accounts can be a highly effective way to reduce your taxable income. Contributions to tax-deferred accounts, such as a Traditional IRA, 401(k), or SEP IRA, are generally deductible on your tax return. By regularly contributing to these accounts, you lower your current taxable income and may qualify for a variety of tax credits.

It’s essential to track your contributions to these accounts and be aware of contribution limits, which may change each year. Not only does this reduce your tax liability, but it also helps you save for your future. For instance, if you contribute the maximum allowed to your 401(k), you can reduce your taxable income by up to $22,500 (in 2024). If you’re self-employed, a SEP IRA offers even larger contribution limits, making it an ideal option for business owners.

Furthermore, if you’re over 50, you may qualify for catch-up contributions, which allow you to save even more for retirement while reducing your taxable income. Staying aware of these opportunities can make a significant difference in your tax preparation efforts and your long-term financial security.

6. Regularly Review Your Financial Statements—Spot Issues Early

As part of your year-round tax season preparation, it’s crucial to regularly review your financial statements. This step is especially important for businesses and self-employed individuals, but it’s also beneficial for those with personal finances to track. At least quarterly, take the time to look over your income, expenses, and profit margins. This habit allows you to catch any discrepancies early and make adjustments before tax season.

For business owners, financial statements such as balance sheets and profit and loss (P&L) reports can provide an overview of your business’s financial health. By reviewing these reports, you can identify trends, see where you may be overspending, and ensure that you’re on track with your financial goals. Regular reviews help you plan for tax payments and understand how much money you’ll need to set aside, which ultimately keeps you on top of your financial situation.

Conclusion

Tax season preparation doesn’t have to be stressful, and the more proactive you are throughout the year, the easier it will be when the time comes. By staying organized, tracking expenses, setting aside money for taxes, and staying updated on deductions and credits, you will find yourself ready to handle tax season with confidence. Don’t wait until the last minute—start implementing these strategies now, and you’ll experience less stress and more financial clarity.